Exploring the Divided Self of Economics: A Challenge to ‘Homo Economicus’

- Understand why the mainstream economic assumption of a ‘rational human’ is criticized.

- Learn core behavioral economics theories (prospect theory, nudges, etc.) through concrete examples.

- Grasp how the conflict and integration between the two economics impact our lives and policies.

I. Two Faces of Economics: Rational Human vs. Real Human

Mainstream economics in the 20th century assumed ‘Homo Economicus’, an idealized human who maximizes self-interest based on economic rationality. This ’economic man’ processes all information perfectly and makes optimal choices based on perfect rationality and self-interest.

Of course, this is far from reality. However, this assumption was a ‘methodological necessity’ to mathematically model complex economic phenomena and establish predictable theories. Thanks to this, powerful analytical tools like the laws of supply and demand and market equilibrium theory could develop. Behavioral economics brings back the reality of ‘humans’—which had been sacrificed for theoretical elegance—into the center of economics.

Events like the 2008 global financial crisis shook the belief in rational markets. Repeated ‘anomalies’ such as market bubbles and crashes, which rational theories alone could not explain, increased calls to include psychological factors in economic analysis.

This gave rise to Behavioral Economics, which borrows insights from psychology and cognitive science to explore how ‘real humans (Homo Sapiens)’ make decisions influenced by emotions and biases.

II. Dawn of Behavioral Economics: Discovery of ‘Bounded Rationality’

The intellectual roots of behavioral economics trace back to 1978 Nobel laureate Herbert A. Simon, who studied human decision-making from a realistic perspective across multiple disciplines.

Simon’s key contribution was the concept of ‘Bounded Rationality.’ Due to limits in cognitive capacity and information search, humans do not seek an ‘optimal solution’ through ‘optimizing’ but instead follow a ‘satisficing’ principle, finding alternatives that are ‘good enough’ to meet minimum criteria.

This was revolutionary because it revealed that human irrationality is not due to fickle emotions but a systematic phenomenon arising from the mismatch between ‘problem complexity’ and the brain’s finite processing ability. This opened a new research field of ‘predictable irrationality.’

III. Why Do Humans Make Irrational Choices?

Building on Simon’s foundation, psychologists Daniel Kahneman and Amos Tversky experimentally demonstrated that human irrationality follows predictable patterns called ‘systematic biases.’

3.1. Prospect Theory: A New Standard for Value Judgment

Prospect Theory is the core theory of behavioral economics.

Advertisement

- Reference Point: People subjectively evaluate value based on ‘gains’ and ’losses’ relative to their current state, not the absolute amount of final wealth.

- Loss Aversion: The pain from losses is about 2 to 2.5 times stronger than the pleasure from equivalent gains. This explains why we are sensitive to losses and prefer maintaining the status quo.

- S-shaped Value Function: Value judgments follow an asymmetric ‘S-shaped’ curve, becoming less sensitive to changes as gains or losses grow larger.

Table 1: Comparison of Key Assumptions between Expected Utility Theory and Prospect Theory

| Feature | Expected Utility Theory | Prospect Theory |

|---|---|---|

| Basis of Value Evaluation | Absolute level of final wealth | Gains/losses relative to reference point |

| Attitude toward Risk | Consistent risk aversion | Risk-averse in gains, risk-seeking in losses |

| Value Function | Concave function | Asymmetric S-shaped function relative to reference point |

| Sensitivity to Gains and Losses | Symmetric | About 2–2.5 times more sensitive to losses (loss aversion) |

| Probability Weighting | Linear weighting of objective probabilities | Overweights low probabilities, underweights high probabilities |

3.2. Framing Effect: How Problem Presentation Determines Choice

The ‘Framing Effect’ describes how choices differ depending on how the same problem is presented. The ‘Asian disease problem’ experiment is a classic example.

- Positive Frame (‘200 people will be saved’): 72% choose the sure option (risk-averse)

- Negative Frame (‘400 people will die’): 78% choose the uncertain option (risk-seeking)

Though mathematically identical, preferences reversed completely depending on whether the frame emphasized ‘saving’ (gain) or ‘dying’ (loss). This strongly evidences that human choices are influenced more by psychological reference points than rational calculation.

3.3. Anchoring Effect and Heuristics

The ‘Anchoring Effect’ is a bias where initial information acts as an ‘anchor’ that distorts subsequent judgments. An experiment showed that irrelevant lucky wheel numbers influenced estimates of the proportion of African countries in the UN.

These effects demonstrate that humans rely on mental shortcuts, or ‘heuristics,’ rather than logic when solving complex problems.

3.4. Endowment Effect: The Value of What Is Ours Is Different

The ‘Endowment Effect’ is the phenomenon where people value items they own much higher than if they do not own them. I have personally felt tempted to price my used items higher than market value when selling.

This clearly shows how loss aversion manifests in reality.

In Richard Thaler’s ‘mug experiment,’ students who owned mugs asked for an average of $5.25 to sell them, while buyers offered only $2.75. The value nearly doubled simply because it was ‘mine.’ Selling the mug was perceived as a ’loss’ of ownership.

Table 2: Summary of Major Behavioral Biases

| Bias | Definition | Canonical Experiment | Real-World Example |

|---|---|---|---|

| Framing Effect | Judgments and choices change depending on the presentation frame | Asian disease problem | ‘10% fat’ vs. ‘90% lean’, 90% surgery success vs. 10% mortality |

| Anchoring Effect | Initial information serves as a reference point influencing subsequent judgments | Lucky wheel and African country estimate | First offer price in negotiations, ‘regular price’ vs. ‘discount price’ tags in stores |

| Endowment Effect | Valuing owned items higher than non-owned | Mug experiment | Pricing own used car higher, hesitation to sell stocks |

| Status Quo Bias | Tendency to maintain current state without special reason | Default options in pension plans | Delaying subscription cancellations, sticking to usual restaurants |

| Mental Accounting | Assigning different values based on money source or use | Lost cash vs. lost movie ticket | Spending ‘found money’ easily but saving salary carefully, conservative management of retirement funds |

IV. Financial Markets: Clash Between the Efficiency Myth and Behavioral Finance

The fiercest battleground between rationalism and behavioralism is financial markets. The mainstream economic ‘Efficient Market Hypothesis (EMH)’ claims asset prices instantly and fully reflect all available information. According to this theory, no one can consistently outperform the market average.

Advertisement

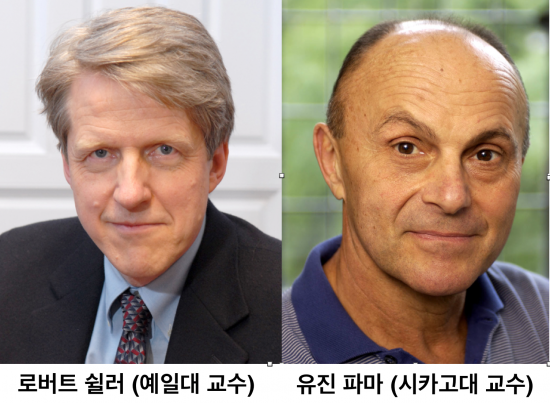

However, phenomena like the dot-com bubble and financial crises are hard to explain with EMH. Behavioral finance scholars like Robert Shiller demonstrated ’excess volatility’—stock price fluctuations are too large to be explained solely by changes in intrinsic value.

Behavioral finance explains that investor overconfidence, herd behavior, and representativeness heuristics create ‘irrational overheating’ that forms bubbles.

The joint award to EMH founder Eugene Fama and its critic Robert Shiller in 2013 is symbolic. It suggests that markets are efficient in the short term (Fama) but vulnerable to massive bubbles and crashes driven by investor psychology in the long term (Shiller), highlighting the need for both views.

V. Sharp Criticisms of Behavioral Economics

Despite its success, behavioral economics faces several criticisms:

- Fragmented Theory: It is often seen as a list of biases without a unified theory. Predicting which bias will appear in which situation is difficult.

- Limited Predictive Power: Excels at explaining past behavior but criticized for lacking quantitative ability to predict future behavior.

- Laboratory Limitations: Questions about the ’external validity’ of controlled lab results applying to complex real markets.

- Role of Learning and Markets: Counterarguments suggest individuals learn from mistakes, and markets weed out irrational actors, enabling long-term rational functioning.

VI. The Soft Power Changing the World: The Pros and Cons of ‘Nudge’

Behavioral economics insights have greatly influenced real-world policy through the ‘Nudge’ theory. Nudges gently steer people toward better decisions by changing choice architecture without coercion or bans.

- Policy Examples: Increasing retirement savings by switching to ‘opt-out’ enrollment, or raising tax compliance by adding messages like “90% of your neighbors have already paid” on tax bills.

- Ethical Debate: Nudges spark debate between respecting individual freedom (’libertarian paternalism’) and state intervention for better lives (‘benevolent paternalism’). Critics worry nudges could become subtle ‘manipulation’ infringing on autonomy.

Ultimately, the nudge debate reveals a fundamental dilemma between individual autonomy and community welfare.

Conclusion

- Key Takeaways

- Limits of Rationality: The traditional ‘Homo Economicus’ differs from reality; humans have ‘bounded rationality’ under cognitive constraints.

- Predictable Irrationality: Behavioral economics proves human irrational behavior is systematic and predictable through prospect theory, framing effects, etc.

- From Conflict to Integration: Behavioral economics does not replace mainstream economics but enriches it with psychological insights for greater explanatory power.

- Call to Action (CTA) What psychological biases have been hidden in your consumption or investment decisions today? Explore behavioral economics principles in daily life and consider making better choices.

References

- Economics and the World: Homo Economicus - Yeongnam Ilbo

- Economic Man - Wikipedia

- Behavioral Economics | Norio Domono - Kyobo Bookstore

- Homo Economicus Hesitates Before Choice - University Newspaper

- Philosophical Reflection on Economic Rationality Concept* - Seoul National University Humanities Institute

- Behavioral Economics - Namu Wiki

- Economic and Financial Humans in College Entrance Exams Are Not Rational…Breaking Traditional Economic Framework - Hankyung Saenggle Saenggle

- Prospect Theory - Wikipedia

- Efficient Market Hypothesis - Wikipedia

- Unfinished Debate on Efficient Market Hypothesis Seen Through Nobel Prize in Economics - Heyri Fund Service

- Criticisms of Behavioral Economics - Economics Online

- Nudge: Final Edition - Aladin