The Psychological Shield of Value Investing Through Behavioral Economics

- Understand why markets systematically overreact due to investors’ psychological biases.

- Learn how Benjamin Graham’s ‘Margin of Safety’ and PER principles act as shackles preventing emotional investing.

- Discover the importance of sticking to principles through the dot-com bubble example and how to apply them in modern contexts.

Is the Market Truly Rational? Efficient Market Hypothesis vs. Behavioral Economics

Traditional financial economics is built on the Efficient Market Hypothesis (EMH), which claims that all information is instantly reflected in stock prices, making it impossible to beat the market and the best strategy is to follow the entire market. This views the market as a perfect calculator.

However, investment masters like Benjamin Graham long ago recognized that markets are not always rational. This insight aligns with modern behavioral economics, which starts from the premise that investors are ordinary humans influenced by emotions and biases, leading to predictable market inefficiencies.

So which perspective should we follow? This article will show that the market is a place of systematic overreactions caused by investors’ psychological biases, and that Benjamin Graham built a perfect investment philosophy decades ago to defend against this.

Why Do Investors Overreact in the Market?

Investor overreaction is not random error but a systematic phenomenon rooted in deeply ingrained cognitive biases. These psychological traps are especially prominent in the complex and uncertain stock market.

Four Psychological Traps That Fuel Overreaction

- Representativeness Heuristic and Anchoring: Investors generalize short-term high growth rates over recent quarters as permanent traits of a company. Simultaneously, they anchor on recent flashy news or soaring stock prices, ignoring the company’s long-term fundamentals.

- Confirmation Bias: Once believing “This company is a revolutionary innovator,” investors tend to seek only information that supports this belief and ignore contradictory data. I myself experienced significant losses early on by only looking for positive news about a single stock.

- Herd Mentality: The tendency to follow others’ actions rather than one’s own analysis. This creates a positive feedback loop where rising prices justify buying, which pushes prices even higher, detaching stock prices from reality.

- Loss Aversion: The pain of losses is felt much more intensely than the pleasure of gains. This leads to irrational behaviors like holding onto winning stocks too long to avoid realizing losses when prices fall.

These biases were empirically proven by De Bondt and Thaler’s 1985 study, known as the “Winner-Loser Effect.” The finding that past “loser portfolios” outperform future “winner portfolios” strongly evidences investors’ excessive overreaction to past performance.

Benjamin Graham’s Antidote: Taming Market Madness

Benjamin Graham penetrated the fickle nature of markets and built a behavioral management system to control it. His philosophy is designed so investors are not swept away by emotional market waves but instead use them to their advantage.

How to Use the Bipolar Partner ‘Mr. Market’

Graham’s “Mr. Market” allegory perfectly depicts the emotional nature of markets. Mr. Market is a bipolar business partner who shows up daily, offering to buy or sell stocks at absurdly high or low prices.

A wise investor does not act on his moods. The key is to buy when Mr. Market is pessimistic and selling stocks cheaply, and sell when he is greedy and offering overpriced shares. This revolutionary perspective redefines market volatility as an “opportunity” rather than a “risk.” How do you respond to Mr. Market’s offers?

The Ultimate Shield: Margin of Safety

The cornerstone of Graham’s philosophy is the “Margin of Safety.” It means buying stocks at prices significantly below their intrinsic value—“buying a $1 asset for 50 cents.”

Advertisement

Margin of Safety acts as a buffer against analysis errors and a cushion against unpredictable market fluctuations. Buying at a sufficiently low price fundamentally prevents the mistake of paying too much in overheated markets.

Behavioral Shackles: The PER Principle

Graham’s philosophy translates into concrete behavior through the Price-to-Earnings Ratio (PER). PER is the stock price divided by earnings per share (EPS), representing the time needed to recover the investment. For Graham, PER was not just a reference but a behavioral shackle controlling investor emotions.

He proposed uncompromising quantitative rules for the “defensive investor”:

- Rule 1: PER should not exceed 15. (Based on the average earnings of the past 3 years)

- Rule 2: The product of PER and PBR (Price-to-Book Ratio) should not exceed 22.5.

These rules act as an automatic “circuit breaker” against speculative frenzies. No matter how dazzling a growth story is, stocks exceeding these limits are excluded from purchase. This fundamentally prevents investors from succumbing to herd mentality and confirmation bias and joining bubbles.

Proof of Madness: The Dot-com Bubble and Graham’s Principles

Nothing illustrates investor overreaction and the defensive power of Graham’s principles more clearly than the dot-com bubble. In the late 1990s, the market was captivated by the “New Economy” narrative, ignoring traditional metrics like profits and assets.

At the time, the average PER of Nasdaq companies reached about 90, and popular tech stocks exceeded hundreds. When the bubble burst in March 2000, the Nasdaq index plunged about 78%. What if an investor had strictly followed Graham’s principles? They would have avoided nearly all popular tech stocks and preserved capital safely while speculators went bankrupt.

Table 1: Overreaction and Correction During the Dot-com Bubble

| Metric | Bubble Peak (circa 1999-2000) | Graham’s Principle Limit |

|---|---|---|

| Nasdaq Average PER | About 90 | Under 15 |

| Popular Tech Stocks PER | 200 to Infinite | Under 15 |

This table clearly shows the huge gap between market madness and Graham’s principles at the time.

Comparison / Alternatives

Evolution of Graham’s Principles: Peter Lynch’s GARP Strategy

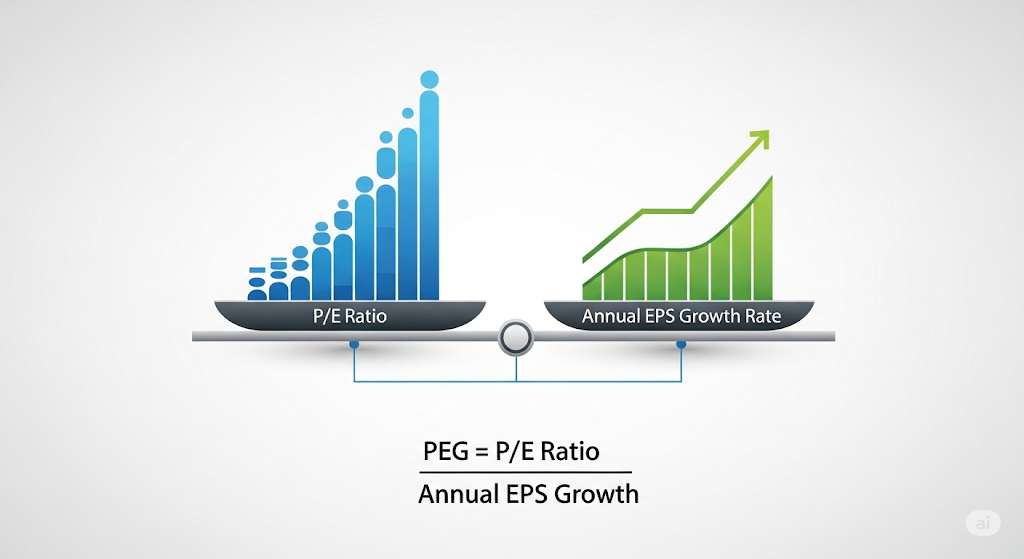

Graham’s strict low-PER strategy has the limitation of potentially missing great growth companies. The legendary fund manager Peter Lynch addressed this dilemma by introducing the concept of “Growth at a Reasonable Price (GARP).”

Advertisement

Lynch’s key tool was the Price/Earnings to Growth (PEG) ratio, calculated as PER divided by annual EPS growth rate (PEG = PER / EPS growth rate), evaluating PER in the context of growth. Lynch considered PEG below 1 as attractively undervalued.

This inherits Graham’s “Margin of Safety” spirit but extends the criteria from current value to future growth potential.

Table 2: Comparative Analysis of Quantitative Value Principles

| Criterion | Benjamin Graham (Deep Value) | Peter Lynch (GARP) |

|---|---|---|

| Main Indicator | PER, PBR | PEG Ratio |

| PER Allowance Range | Low (strictly under 15) | Moderate (acceptable if justified by growth) |

| Core Philosophy | “Margin of Safety” | “Growth at a Reasonable Price” |

Checklist

Benjamin Graham-style Checklist for Trained Investors

Before investing, ask yourself:

- Is this an ‘investment’ or ‘speculation’?: Is there thorough analysis ensuring principal safety and satisfactory returns?

- Is the ‘Margin of Safety’ secured?: Are you buying at a price significantly below intrinsic value?

- Does it meet quantitative criteria?: Is PER under 15 and (PER × PBR) under 22.5?

- Are you swayed by ‘Mr. Market’s’ emotions?: Are decisions based on your analysis and principles rather than market mood?

Conclusion

The stock market is not a rational machine but a vast battlefield shaped by human psychological biases. Benjamin Graham’s investment philosophy is a powerful defense system protecting investors in this psychological war.

Key Takeaways

- Markets are irrational: Investors systematically overreact due to cognitive biases like representativeness heuristic, confirmation bias, and herd mentality.

- Principles beat emotions: Graham’s PER rules are not mere indicators but behavioral controls shielding investors from market madness.

- Training beats prediction: Whether strict Graham rules or flexible Lynch PEG ratios, the core is a trained attitude that excludes emotions and adheres to quantitative principles.

Ultimately, surviving market noise is not about being the smartest forecaster but the most disciplined investor. May this article help you establish your own investment principles and focus on numbers, not market stories.

References

- Wikipedia, Efficient-market_hypothesis

- Ministry of Economy and Finance, Efficient Market Hypothesis - Economic Terms Dictionary

- Namu Wiki, Efficient Market Hypothesis

- Brunch, Introduction to Behavioral Economics - The Meeting of Economics and Psychology

- KDI Economic Information Center, Exploring Human Psychology through Behavioral Economics

- Wikipedia, Cognitive Bias

- Kyobo Bookstore, Empirical Study on Contrarian Investment Strategies in the Chinese Stock Market

- Steemit, Benjamin Graham’s Timeless Investment Principles

- SPI, Benjamin Graham, the Beginning of Securities Factor Analysis

- TopClass, Benjamin Graham, the Father of Value Investing

- Yes24, The Intelligent Investor by Benjamin Graham

- Alpha Square, Insight Post

- YouTube, Mastering PER (Price-to-Earnings Ratio) in 10 Minutes

- Korea Investment & Securities, Benjamin Graham

- Newspim, 2000 IT Bubble and 2018 KOSDAQ… “Is This Time Different?”

- Chosun Ilbo, Fear of a Second IT Bubble… What’s Different Between 2000 and 2020

- Yonhap News, Dot-com Bubble Nightmare Revived Amid U.S. Stock Market Slump… “Incomparable” Evaluation

- Shindonga, Peter Lynch’s Lifestyle Growth Stock Strategy That Led to Retirement at 46