Uncovering the deadly risks hidden behind the sweetness of ‘zero’ brokerage fees.

- Why direct real estate transactions have exploded

- Three common types of fraud in direct transactions

- Essential checklist for safe direct transactions

The Story of Two Tenants

Here are two young people. One is Minjun, a graphic designer in his 30s. He recently found a perfect one-room apartment in Mangwon-dong through Danggeun Market. By contracting directly without a licensed broker, he saved over 1 million KRW in brokerage fees, known as ‘bokbi’. He proudly tells his friends, “A little legwork saved me this much money.” Minjun’s story is the sweet success promised by direct real estate deals.

The other is Sujin, a recent graduate stepping into society. She also found a great house below market price on a platform. The ‘landlord’ was friendly, and everything seemed smooth. Without hesitation, Sujin transferred her entire lease deposit, which her parents had saved their whole lives for. But on moving day, she was met with a cold locked door and a ‘ghost landlord’ who disappeared without contact. Sujin’s story reveals the devastating risks hidden behind the rosy illusion of direct transactions.

These two stories are not extreme fiction. They reflect realities unfolding right now in South Korea’s real estate market. This article asks you: “Is saving that brokerage fee worth gambling your entire deposit?” By the end, you will clearly understand the stakes, rules of this game, and how to be Minjun, not Sujin.

Chapter 1: The Sweet Temptation of ‘Zero Brokerage Fees’

The New Era of Digital Real Estate

In the past, direct real estate transactions were exceptional cases, mostly between family or special relations. But now it’s different. With a smartphone app, you can trade multi-million won homes as easily as used furniture. Especially, direct real estate deals through secondhand platforms like ‘Danggeun’ have exploded.

The numbers prove the change. In 2021, only 268 real estate transactions occurred via the Danggeun app; by 2023, this soared to 59,451—an increase of 220 times in just three years. Listings also increased 124-fold. This is not just a new trend but a revolution in how people find homes. Platforms like ‘Peter Pan’s Good Room Search’ and ‘Jip Panda’ have accelerated this trend, making real estate information accessible to everyone.

The Core Motive: The Huge Barrier of ‘Brokerage Fees’

At the heart of this change is a simple but powerful motive: the desire to save money. With soaring home prices, brokerage fees calculated as a percentage of the transaction amount have become a significant burden. The urge to “save on fees” drives many into the direct transaction market.

So how much can you save? The table below shows the maximum brokerage fees tenants pay under current legal rates for lease contracts.

Housing Lease Brokerage Fee Rates (Tenant’s Maximum Fee Example)

| Transaction Type | Converted Deposit | Maximum Rate | Tenant’s Maximum Fee (Including 10% VAT) |

|---|---|---|---|

| Monthly Rent | 150 million KRW (e.g., 50 million deposit / 1 million monthly rent) | 0.3% | 495,000 KRW |

| Jeonse (Lump-sum Lease) | 200 million KRW | 0.3% | 660,000 KRW |

| Jeonse | 500 million KRW | 0.3% | 1,650,000 KRW |

| Jeonse | 800 million KRW | 0.4% | 3,520,000 KRW |

Reasons Beyond Money

Direct transactions also appeal because of ‘speed’ and ‘control.’ In a sluggish market, landlords prefer to list properties directly on platforms to find tenants faster rather than waiting for brokers. Tenants, especially the MZ generation familiar with apps like ‘Hogangnono,’ want to choose properties themselves rather than rely on brokers. Negotiating price and terms directly increases the chance of mutual satisfaction.

Advertisement

However, behind these conveniences lies a trap we often overlook. The explosive growth and ease of use of secondhand platforms ironically lower vigilance against high-risk transactions. Real estate contracts involving hundreds of millions of won are complex legal acts requiring expert help. But trading homes in the same user interface as selling an old bicycle makes people forget the gravity of the transaction. Platforms’ slogans like ‘safe neighborly transactions’ and explicit displays of ‘savings from direct deals’ encourage this illusion. The risk hasn’t disappeared; it’s just hidden behind a convenient user experience. This is the biggest blind spot created by the ‘normalization of risk.’

Chapter 2: Wolves in Sheep’s Clothing: Dissecting Direct Transaction Frauds

Harsh Reality in Numbers

Before diving into fraud cases, let’s face reality. Over the past 34 months, 45.8% of domestic real estate transactions were direct deals. Not all are fraudulent, but the scale is huge. Fraud losses in this market reached 1.57675 billion KRW as of October 2024. Let’s see how these cold numbers destroy individual lives through real cases.

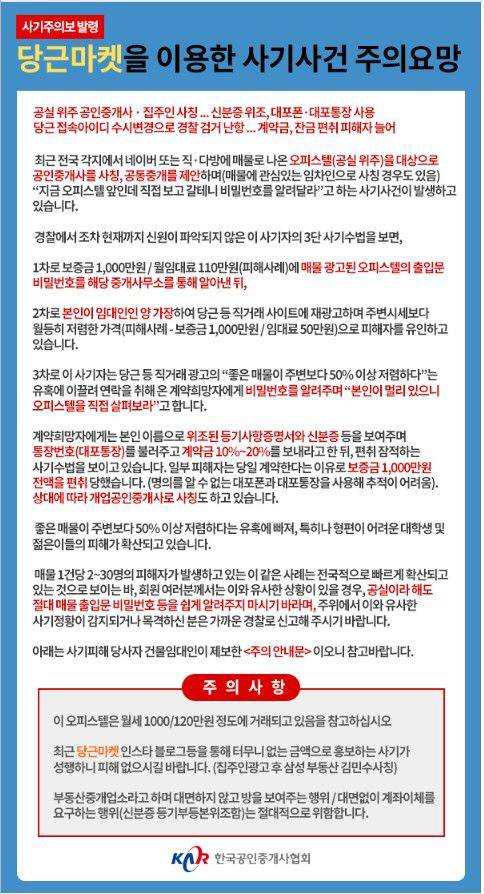

Case 1: The Ghost Landlord

Returning to Sujin’s story from the introduction: she found a newly renovated officetel 20% below market price. The man claiming to be the landlord said he was on a business trip and couldn’t show the house but gave her the door code. After inspecting alone, Sujin was impressed. He sent ID and registry documents via messenger, which looked legitimate.

She hurriedly sent a 5 million KRW deposit and later transferred the full 150 million KRW lease payment. But on moving day, the code had changed, and the landlord disappeared. The real owner was unaware the property was leased. All documents Sujin received were expertly forged, and the scammer had secretly observed the real broker showing the house to steal the door code. This typical fraud exploits platform weaknesses—lack or poor owner identity verification when listing properties.

Case 2: The Devil’s Double Contract

A young couple searching for a newlywed home met a ‘building manager’ claiming authority from the landlord. He showed a genuine power of attorney with the landlord’s seal, reassuring them. They signed a 200 million KRW lease contract with him. But unknown to them, the manager had separately signed a monthly rent contract with the landlord for 20 million KRW deposit and 1.5 million KRW rent. He gave the landlord only the 20 million KRW deposit and absconded with the remaining 180 million KRW. The couple was recognized only as monthly tenants by the landlord, making it nearly impossible to recover their large deposit. This ‘double contract’ fraud highlights the fatal risks of dealing with agents and is a clear criminal offense under criminal law (breach of trust).

Case 3: The Hope-Stealing Key Money Scam

Risks of direct deals are not limited to residential properties. With a surge in commercial property listings due to severe business hardships, ‘key money’ scams have also increased. A young entrepreneur found a prime café listing on a platform. The previous tenant offered a low key money and promised to transfer loyal customers and know-how. The entrepreneur paid tens of millions KRW in key money directly and took over the store. Soon after, the landlord notified that the lease would not be renewed. The landlord had never consented to the tenant transfer, and the supposedly thriving store was actually near closure. This case shows how dangerous tenant-to-tenant direct deals without landlord consent are, and how intangible ‘key money’ can vanish into thin air.

These individual frauds are not isolated stories. They are microcosms of large-scale lease frauds that shook Korean society, like the ‘Villa King’ and ‘Construction King’ cases. Forged documents, deception of ownership, and information asymmetry are core fraud methods used by both organized crime and individual scammers. The rise of online platforms has provided fertile ground for these frauds to spread widely and easily. In other words, the spread of direct transaction fraud via platforms is not a new crime type but a ‘digital popularization’ of existing fraud methods. Behind every small scam you encounter lies a shadow of a massive social disaster.

Chapter 3: The Invisible Shield: What You Give Up Skipping Brokers

Choosing direct transactions is not just about saving brokerage fees. It means forgoing the legal and institutional protections provided by licensed brokers. You must understand how crucial this shield is.

Advertisement

Beyond Guides: Brokers’ Legal Duty to Verify and Explain

The core role of licensed brokers is the ‘duty to verify and explain’ mandated by the Licensed Real Estate Agents Act. This legal responsibility requires brokers to faithfully and accurately explain all important information about the property to clients before contract signing—not just showing the house.

- Basic Information: Address, area, structure, and physical status

- Rights Status: Analyze ownership, mortgages, provisional seizures, priority leases, etc. via registry

- Legal Restrictions: Land use plans, building regulations

- Facilities and Environment: Water, electricity, gas, leaks, noise, sunlight

- Taxes and Costs: Acquisition tax, landlord’s tax arrears, other tenants’ confirmed dates affecting deposit safety

All these checks are documented in an official legal form called the ‘Verification and Explanation Document’ given to parties, with brokers legally responsible for its contents.

Expert Skill: Rights Analysis

‘Rights analysis’ is the professional skill of interpreting complex legal terms in the registry and uncovering hidden risks. For example, identifying ‘pre-registration’ or excessive mortgage amounts that predict future auction risks is the expert’s role. Direct transactions mean you must perform all this analysis yourself.

Safety Net and Its Flaws: The Truth About Compensation Certificates

When contracting through a broker, you receive a ‘compensation certificate’—a kind of insurance that compensates clients for damages caused by the broker’s intentional or negligent acts. Currently, individual brokers’ coverage is up to 200 million KRW, corporations up to 400 million KRW. Many mistakenly believe this guarantees full compensation up to these amounts. This is a dangerous misconception. The reality:

- Lawsuit Required: You must first win a damage claim lawsuit proving the broker’s fault.

- No 100% Compensation (Comparative Negligence): Courts usually hold clients partly responsible, so actual compensation averages only 55.9% of the claim.

- Most Fatal Trap (Total Limit): The 200 million KRW limit is not per incident but the total amount the broker can pay in a year.

In conclusion, the compensation certificate is not personal insurance for tenants but a minimal professional liability insurance for brokers.

Platforms Avoid Responsibility: ‘We’re Just a Bulletin Board’

Unlike brokers who bear heavy legal responsibility, direct transaction platforms generally disclaim any responsibility for problems arising during transactions. They define themselves as ‘information bulletin boards’ only. There is no official channel to mediate or resolve issues, and all responsibility falls solely on the parties involved.

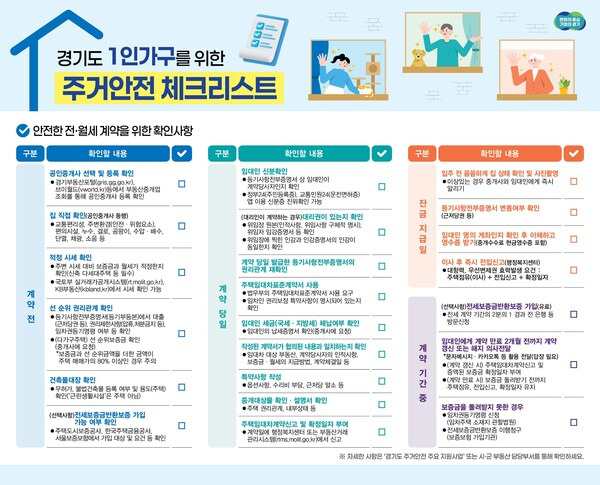

Chapter 4: The Ultimate DIY: A Complete Guide to Safe Direct Transactions

If you decide to take all these risks, you must become your own licensed broker. The following steps are mandatory; missing any can cost you everything.

Step 1: War with Documents – Become Your Own Analyst

Obtain Essential Documents

- Registry Copy (Full Registration Certificate): Available at Supreme Court Internet Registry (www.iros.go.kr).

- Building Register: Free at Government24 (www.gov.kr).

Perfectly Dissect the Registry Copy

- Title Section: Confirm the exact address, building, and unit number match the contract.

- Section A (Ownership): Verify the current owner matches the landlord’s ID. Stop immediately if you see terms like ‘provisional seizure,’ ‘seizure,’ ‘injunction,’ or ‘auction.’

- Section B (Other Rights): Check mortgage amounts. If (maximum mortgage claim + your deposit) exceeds 70–80% of the home’s market price, the risk of ‘empty lease’ is very high.

Check the Building Register

- Confirm the building’s exact use (e.g., residential, neighborhood facility).

- Check for ‘illegal building’ marks in the top right corner. Illegal buildings may be rejected for lease loan applications.

Clearly Understand the Relationship Between the Two Documents

The registry proves rights (who owns the property), while the building register proves facts (what the building is). Ownership is confirmed by the registry; address, area, and physical status by the building register. Cross-check both for consistency.

Registry Copy vs Building Register Comparison

| Item | Registry Copy (Rights Document) | Building Register (Fact Document) | Which Takes Priority? |

|---|---|---|---|

| Ownership | Final confirmation basis | Owner info recorded | Registry Copy |

| Address, Area, Use | Recorded | Final confirmation basis | Building Register |

| Loans, Seizures | Only source | Not recorded | Registry Copy |

| Illegal Construction | Not recorded | Only source | Building Register |

Step 2: Verify the Person – Is Your Landlord Real?

Simply looking at the landlord’s ID is meaningless. Fake IDs are common. You must verify authenticity through government systems.

Advertisement

Verify ID authenticity via Government24 or ARS 1382.

- Method 1 (Phone): Call 1382 without area code, enter resident registration number and issue date.

- Method 2 (Online): Use ‘Resident ID Authenticity Check’ service on Government24 (www.gov.kr).

This must be done on-site at contract signing, in front of the landlord, stamping the contract.

Step 3: Use the Contract as Armor – How to Use Special Clauses

A standard lease contract alone won’t protect you. ‘Special clauses’ are your strongest shield. Include these mandatory clauses:

- Essential Clause 1 (Prevent Dangerous Gaps): “The landlord shall maintain the rights status on the registry as of contract date until the day after the final payment; if violated, the tenant may immediately cancel the contract and the landlord must refund the full deposit immediately.”

- Essential Clause 2 (Exit if Loan Fails): “This contract is conditional on the tenant’s lease loan approval; if loan is denied due to landlord or property defects, the contract is void and the landlord must refund the full deposit immediately.”

- Essential Clause 3 (Deposit Return Guarantee): “At lease expiration, regardless of new tenant status, the deposit shall be returned immediately on the expiration date.”

Step 4: Plant Your Flag – Secure Your Legal Rights

Signing the contract is not the end. The final step is legally securing your rights.

- The Tenant’s Protection Trinity: Your deposit is protected by ① Occupancy (moving in and living), ② Moving-in Report, ③ Confirmed Date Stamp.

- Moving-in Report: Report within 14 days at local community center or Government24. This grants you ‘opposability’—the right to stay even if ownership changes.

- Confirmed Date Stamp: Get a date stamp on the original contract. This grants ‘priority repayment right’ to get your deposit back before other creditors if the property is auctioned.

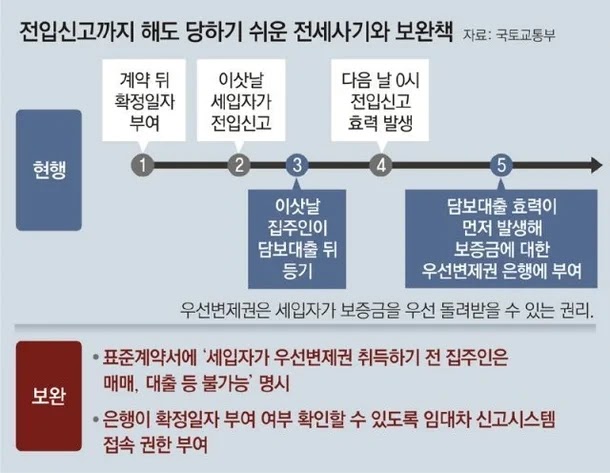

The Most Important Warning: The ‘Dangerous Day’ Exists

The effect of the moving-in report starts at 0:00 the day after the report, a loophole exploited by fraudsters.

Here lies the fatal trap. Your opposability and priority repayment rights only take effect from 0:00 the day after you complete moving-in and the moving-in report. If a malicious landlord takes out a mortgage on the afternoon of your move-in day, the bank’s mortgage will legally have priority over your lease rights. This is why ‘Essential Clause 1’ above is life-critical.

Conclusion: Calculated Risk or Reckless Gamble?

We return to the initial question: Is it okay to contract real estate without a licensed broker? This article does not give a simple yes or no. Instead, it clarifies what this choice means.

- Key Point 1: Direct transactions clearly save brokerage fees and give control but the convenient UI makes people forget the risks.

- Key Point 2: Fraud methods like ghost landlords and double contracts are increasingly sophisticated and can ruin you financially.

- Key Point 3: To transact safely, you must perfectly handle registry analysis, ID verification, essential contract clauses, moving-in report, and confirmed date stamp yourself.

On one side of the scale is the definite, sweet benefit of saving tens or hundreds of thousands of KRW in fees; on the other is the risk of losing your entire deposit worth hundreds of millions.

Advertisement

Having read this, you now know the true nature of the risks and hold the tools to analyze and avoid them. Whatever you choose, may you walk not blindly in the fog but with clear eyes seeing all.

References

- [Exclusive] “Must save 6 million won in fees” Direct real estate transactions surged 220 times in 3 years [Buying a house with an app①] - Daum Link

- [Kim Seulgi’s Friendly Real Estate] Direct deals on ‘Danggeun’ to save fees? Check ‘this’ Link

- Saving on salary, “Selling our house”… Why ‘Danggeun Real Estate’ exploded / SBS 8 News - YouTube Link

- [Minji Review] From real estate ‘sucker’ to ‘expert’… MZ generation’s favorite real estate info apps | JoongAng Ilbo Link

- [Easy Real Estate] Evolution and countermeasures of direct transaction fraud - Daum Link

- “Contracted and paid, but…” Real estate ‘direct transaction fraud’ goes this far (subtitled news) / SBS - YouTube Link

- Brokerage contracts and licensed brokers’ responsibilities - Easy Law Info Link

- Compensation for damages caused by brokers is about half the claim - Tax Accountant Newspaper Link

- Government24 Resident ID Authenticity Check Link

- Housing Lease - Acquisition of opposability and priority repayment rights - Easy Law Info Link