The Epic of Interest Rates, Inflation, and Crisis Response

- How the U.S. Federal Reserve (Fed) was born and how its role has evolved

- The key decisions the Fed made during major economic crises like the Great Depression, stagflation, and the 2008 financial crisis

- How the Fed’s policies directly affect our mortgage rates, investments, and prices today

If this morning you checked your mortgage interest rate, worried over stock market fluctuations, or sighed at soaring grocery prices, you have already stepped into the vast story of the U.S. Federal Reserve (Fed). Decisions made in Washington D.C. are invisibly linked to our wallets, investments, and future.

The Fed’s history is not just a list of economic policies. It is a dramatic saga of power, failure, and adaptation. This article traces over 110 turbulent years of the Fed’s history, revealing how a series of massive crises forged it from a limited financial safety net into the world’s most powerful economic institution.

The Birth of a Giant: The Panic of 1907 and the Fed’s Founding

An Era Without a Central Bank

At the turn of the 20th century, the U.S. was at the peak of the Gilded Age, a massive industrial powerhouse dominated by steel and railroads. Yet behind this splendor lay a fatal weakness: the absence of a central bank.

At the time, the money supply was tied to the amount of government bonds banks held, creating an ‘inelastic currency’ that could not flexibly adjust to economic conditions. This exposed the entire financial system to periodic panic risks.

J.P. Morgan, the Crisis Savior

In October 1907, a speculative failure triggered a bank run on Wall Street, pushing the financial system to the brink of collapse. Even the New York Stock Exchange faced bankruptcy.

At this critical moment, the era’s top financier J. P. Morgan (John Pierpont Morgan) stepped in as a savior. He deployed his own capital and pressured other bankers to form a bailout fund, effectively performing the role of a central bank single-handedly.

This event exposed the uncomfortable truth that the fate of the U.S. economy rested in the hands of a single private individual, sparking political demands for a central bank.

The Federal Reserve Act: A Compromise

Amid political tensions, the Federal Reserve Act was enacted in 1913. Instead of a single central bank like in Europe, the U.S. devised a decentralized ‘system’ dividing the country into 12 districts, each with a regional Federal Reserve Bank.

The Fed’s initial mission was less about macroeconomic management and more like a financial plumber.

Advertisement

- Elastic currency supply: Providing cash to prevent bank runs

- Lender of last resort: Supporting bank liquidity through the ‘discount window’

- Payment system improvements: Simplifying check clearing procedures

Crucially, modern concepts like ‘monetary policy,’ ‘maximum employment,’ and ‘price stability’ did not yet exist.

The Great Depression: The Fed’s Darkest Hour (1929–1950)

The Roaring Twenties and Seeds of Disaster

After World War I came the economic boom known as the Roaring Twenties. The Fed raised interest rates in 1928 and 1929 to curb speculative excesses, but economist Milton Friedman later argued this triggered the recession.

Fatal Inaction and the “Original Sin”

Following the 1929 stock market crash, a wave of bank failures swept the U.S. through 1933. At this critical juncture, the Fed betrayed its very purpose.

Instead of acting as the lender of last resort, the Fed largely stood by as thousands of banks collapsed. This ‘great betrayal’ caused the money supply to shrink by one-third, drying up the economy’s lifeblood and triggering a vicious cycle of mass unemployment. This event is recorded as the Fed’s ‘original sin.’

Cause of Failure: Flawed Doctrine

The Fed’s impotence was not due to lack of tools but because of flawed beliefs dominating its mindset.

- Real Bills Doctrine: The belief that rescuing banks failing due to speculative assets was not the central bank’s role.

- Blind faith in the Gold Standard: To prevent gold outflows, the Fed raised interest rates sharply amid economic collapse—akin to pouring gasoline on a burning house.

Later, Milton Friedman and Anna Schwartz declared in “A Monetary History of the United States” that the Great Depression was not capitalism’s failure but the government’s, especially the Fed’s. This painful lesson profoundly influenced later Fed Chairman Ben Bernanke’s crisis response.

After this devastating failure, the Fed’s stature plummeted, losing independence and becoming effectively a servant of the Treasury Department.

Declaration of Independence: The 1951 Accord and a New Era of Power

Inflation Pressures and Conflict

After World War II, the Fed had to keep government bond yields artificially low to manage massive debt. When the Korean War broke out in 1950, inflation surged, reaching 21% consumer price growth by February 1951.

The Fed wanted to raise rates, but President Harry Truman strongly opposed it. This conflict became public, escalating into a crisis.

Advertisement

The 1951 Treasury-Fed Accord

In March 1951, the historic Treasury-Fed Accord was reached.

- Agreement: The Fed was no longer obligated to keep interest rates fixed at government-set levels.

- Historical significance: Known as the ’liberation of monetary policy,’ this established the Fed’s core principle of independence, enabling it to conduct genuine monetary policy.

Insight: This accord fundamentally rebalanced power between the government (the spender) and the Fed (the controller of money’s value). It gave the Fed the strength to impose short-term pain (rate hikes) for long-term price stability, even if politically unpopular. This independence laid the institutional foundation for Paul Volcker’s inflation fight in the 1980s.

Stagflation and the Birth of the Dual Mandate (1971–1979)

The Collapse of the Phillips Curve and Shocks

Before the 1970s, economists believed in the Phillips Curve theory, which posited a stable inverse relationship between unemployment and inflation. But two major shocks shattered this belief.

- Nixon Shock (1971): President Nixon ended dollar convertibility to gold, severing the last link to the gold standard.

- OPEC Oil Embargo (1973): Oil prices quadrupled, delivering a massive supply shock to the economy.

The Emergence of the Monster ‘Stagflation’

The result was stagflation—the terrible combination of high unemployment and high inflation simultaneously. The economy stagnated while prices soared, plunging the Fed into its worst dilemma.

The Birth of the Dual Mandate

Amid this turmoil, Congress passed a law in 1977 requiring the Fed to pursue both maximum employment and stable prices simultaneously. This became the Fed’s famous dual mandate.

Rather than a clear solution, it was a political compromise that forced the Fed to juggle conflicting goals. This ambiguous responsibility set the stage for the painful choices faced by the next chairman, Paul Volcker.

The Volcker Shock: Taming the Inflation Dragon (1979–1987)

By 1979, U.S. inflation neared 15%, and inflation expectations ran wild. The Fed had lost all credibility.

President Jimmy Carter appointed the tough anti-inflationist Paul Volcker as Fed chairman. Volcker believed shock therapy was necessary to break the vicious cycle of inflation expectations.

The ‘Volcker Shock’ and Painful Victory

In October 1979, Volcker announced a radical shift in monetary policy. The federal funds rate soared to an astonishing 20% by June 1981.

Advertisement

This pushed the U.S. into two deep and painful recessions. Unemployment approached 11%, sparking massive social backlash.

Yet despite the pain, the ‘Volcker Shock’ succeeded. Inflation fell below 3% by 1983. Volcker restored the Fed’s credibility as an independent inflation fighter and laid the foundation for two decades of price stability.

Insight: Volcker chose ‘price stability’ over ‘maximum employment,’ temporarily sacrificing the latter. His success established a powerful precedent equating Fed credibility with its willingness to fight inflation, a legacy carried on by Greenspan, Bernanke, and Yellen.

The Maestro and the Collapse: The Great Moderation to the 2008 Crisis

The Great Moderation and the ‘Greenspan Put’

Following Volcker, Alan Greenspan’s tenure was marked by low inflation and steady growth—the Great Moderation.

However, the Fed repeatedly cut rates to rescue markets during crashes and crises, fostering the belief in a ‘Greenspan Put’—the idea that the Fed would always bail out markets. This encouraged excessive risk-taking by financial institutions.

The 2008 Global Financial Crisis

Eventually, the housing bubble burst, and the September 2008 bankruptcy of Lehman Brothers triggered a global financial panic.

Bernanke’s Response: “We Did It”

Fed Chairman Ben Bernanke, a leading Great Depression scholar, vowed not to repeat the Fed’s 1930s errors and deployed unprecedented policies.

- Zero Interest Rate Policy (ZIRP): Lowered the federal funds rate to near zero.

- Alphabet Soup Bailouts: Provided liquidity not only to banks but also to other critical financial sectors.

- Birth of Quantitative Easing (QE): Created new money to buy massive amounts of long-term Treasury bonds and mortgage-backed securities (MBS), directly lowering long-term interest rates.

Insight: The 2008 crisis response permanently expanded the Fed’s role. It transformed from a traditional bank regulator into the ultimate safety net for the entire financial system and a direct manipulator of long-term asset prices. This marked the start of the ’new normal’ where the Fed’s balance sheet became a key policy tool, setting a precedent for even greater intervention in 2020.

Table 1: The Era of Quantitative Easing (QE1-QE3)

Advertisement

| Program | Announcement/Start Date | Major Assets Purchased |

|---|---|---|

| QE1 | November 2008 | Agency debt and MBS |

| QE1 Expansion | March 2009 | Agency debt, MBS, long-term Treasuries |

| QE2 | November 2010 | Long-term Treasuries |

| QE3 | September 2012 | Long-term Treasuries and MBS |

Note: This table shows how QE evolved from an emergency measure to a deliberate economic stimulus tool.

The Pandemic Panic: The Fed Bets Everything (2020–2021)

The COVID-19 pandemic was a public health crisis that forced the entire economy to a halt at a speed incomparable to 2008.

Led by Chairman Jerome Powell, the Fed immediately pulled out the 2008 playbook but on a much larger scale and speed.

- Back to zero rates: Cut rates to 0% in two emergency meetings.

- Unlimited QE: Effectively declared ‘unlimited QE.’

- Rescuing everything: For the first time, supported corporate bond markets, local governments, and mid-sized companies.

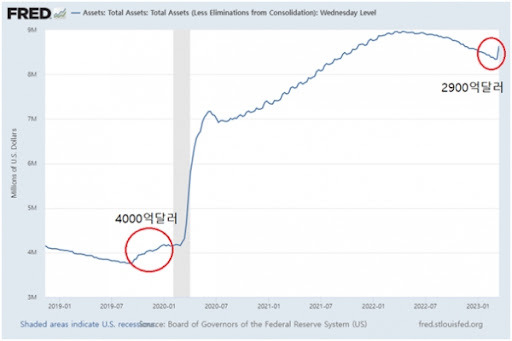

As a result, the Fed’s balance sheet ballooned to nearly $9 trillion by early 2022.

Insight: The 2020 response proved that the Fed’s ‘unconventional’ policies from 2008 had become standard crisis tools. However, by directly supporting corporate bonds and others—traditionally Congress’s domain of credit allocation—the Fed raised fundamental questions about its independence and mission limits.

The Mistake of ‘Transitory’ and a Major Shift (2021–Present)

Inflation Surge and Misjudgment

In 2021, massive stimulus and pent-up demand caused inflation to surge. Led by Powell, the Fed initially labeled this inflation as ’transitory.’ They believed it was due to supply chain bottlenecks, accustomed to a decade of low inflation. In effect, they were fighting the last war.

Humbling Reversal and Aggressive Rate Hikes

By late 2021, as inflation proved more persistent, Powell officially abandoned the word ’transitory.’

The Fed then made a dramatic policy pivot. Starting March 2022, it launched the most aggressive rate hikes in 40 years, raising the federal funds rate from 0% to over 5% within about a year. Simultaneously, it began shrinking its balance sheet through Quantitative Tightening (QT).

Insight: The misjudgment of ’transitory’ reveals the fundamental challenge facing the modern Fed. Powerful tools that successfully prevented deflation ironically sowed the seeds for the next inflation crisis. The Fed may now be trapped in a new cycle. Conquering deflation essentially plants the seeds for the next inflation. Navigating this new world is the Fed’s key challenge going forward.

Advertisement

Conclusion

The Fed’s 110-year history is a journey of continuous evolution driven by crises. Starting as a simple financial plumber, it endured the Great Depression’s failures, was reborn as an independent power, tamed the inflation dragon, and became the ultimate market savior.

Three key takeaways:

- Crises shape the Fed: The Fed’s authority and role expanded dramatically through major crises like the 1907 panic, the Great Depression, and the 2008 financial crisis.

- Trust is earned through struggle: The 1951 independence and the 1980s Volcker shock symbolize the Fed’s hard-won credibility in pursuing long-term stability against political pressure.

- New era, new challenges: Since 2008, the Fed gained immense power to rescue the entire financial system, but this also birthed new inflation risks and complicated policy decisions.

The Fed’s delicate balancing act among inflation control, growth promotion, and financial stability is an ongoing drama. With this historical context, you can better understand future Fed policy decisions and apply this insight to your asset management.

References

- Panic of 1907 - Wikipedia Link

- The Evolution of the Role of the Federal Reserve - Mercatus Center Link

- Overview: The History of the Federal Reserve - Federal Reserve History Link

- [Daehong Kim Column] Why the U.S. Fed is a Corporation… The Birth and Governance Secrets of the FRB - Global Economic Link

- JP Morgan⑧…1907 Financial Panic Acting as Central Bank - Atlas News Link

- 1913 Federal Reserve Act: Definition and Why It’s Important - Investopedia Link

- Federal Reserve System - Namu Wiki Link

- The Great Depression - Federal Reserve History Link

- The Great Depression’s Quagmire④…US Fed’s Major Error, Interest Rate Hike - Atlas News Link

- The Treasury-Fed Accord - Federal Reserve History Link

- Federal Reserve Reform Act of 1977 - Federal Reserve History Link

- Volcker’s Announcement of Anti-Inflation Measures - Federal Reserve History Link

- What did the Fed do in response to the COVID-19 crisis? - Brookings Institution Link