Why Do Value Stocks Deliver Higher Returns Than Growth Stocks? An Unending Debate.

- Understand the logic behind the two key hypotheses explaining the value premium (risk compensation and market overreaction).

- Apply each hypothesis to real-world examples of representative companies (POSCO, Bank of America).

- Explore the reasons behind the recent weakening of the value premium and the lessons investors should learn today.

The Longstanding Puzzle in Finance: What Is the Value Premium?

In finance, there is a fascinating puzzle that has remained unsolved for decades: the value premium phenomenon. Simply put, “value stocks,” which are priced cheaply relative to their intrinsic value, tend to deliver higher long-term returns than “growth stocks,” which are priced for high future growth. This phenomenon challenges the core of traditional finance theory that “higher returns come only with taking greater risk,” making it one of the strongest anomalies.

To solve this puzzle, we will delve deeply into two main perspectives: the “risk compensation hypothesis,” which argues that value stocks earn higher returns because they are inherently riskier, and the “market overreaction hypothesis,” which claims that investors’ psychological biases cause price distortions.

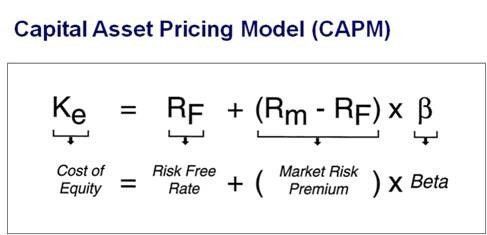

1. The Breakdown of the Traditional Model: Why CAPM Failed to Explain the Value Premium

The cornerstone of modern finance theory, the Capital Asset Pricing Model (CAPM), explains that an asset’s expected return is determined solely by its systematic risk (beta, β), which moves with the overall market.

According to this model, if value stocks have higher returns than growth stocks, their betas must be higher. However, numerous studies have shown the opposite: value stocks with low price-to-book ratios (PBR) consistently outperform growth stocks regardless of beta, and often have lower betas.

This contradiction proved CAPM’s predictions inconsistent with reality and raised the fundamental question: “Is the market inefficient, or are we misunderstanding ‘risk’?”

Table 1: Long-Term Performance of Value vs. Growth Stocks in the U.S. Market (Annualized Returns)

| Period | Value Stock Portfolio | Growth Stock Portfolio |

|---|---|---|

| 1927-2022 | 12.8% | 9.7% |

| 1963-2022 | 13.5% | 10.2% |

| 2000-2022 | 8.9% | 7.1% |

Note: Classified by book-to-market (B/M) ratio based on Fama/French data. Source: Reconstructed from Kenneth R. French Data Library.

2. Hypothesis 1: The Value Premium Is Compensation for “Hidden Risk”

From the perspective of the efficient market hypothesis (EMH), “there is no free lunch.” This hypothesis argues that the value premium is not a market inefficiency but a rational compensation for another systematic risk that CAPM fails to capture.

The Emergence of the Fama-French Three-Factor Model

Eugene Fama and Kenneth French extended the traditional CAPM by adding two factors—size (SMB) and value (HML)—to market risk, creating the ’three-factor model.’

Advertisement

- SMB (Small Minus Big): A risk factor reflecting the ‘size effect,’ where small-cap stocks tend to outperform large-cap stocks.

- HML (High Minus Low): A risk factor reflecting the ‘value effect,’ where value stocks tend to outperform growth stocks.

This model explains over 90% of stock return variations. From this viewpoint, the value premium is a natural reward for bearing the HML risk factor. The HML factor mainly represents financial distress risk and cyclical risk sensitive to economic fluctuations.

Case Study: POSCO and the Fate of Cyclical Value Stocks

A good example of the risk compensation hypothesis is POSCO, a steel company. Although POSCO is a typical value stock, its low PBR can be seen as a rational market assessment of risk.

- Extreme economic sensitivity: The steel industry’s performance heavily depends on the health of downstream sectors like automotive and construction. During recessions, demand plunges, exposing the company to significant systematic risk.

- High operating leverage: Massive fixed assets like steel plants cause profits to fluctuate more dramatically than sales.

The market’s assignment of a low PBR to POSCO reflects a rational pricing of its inherent cyclical risk. Investors demand a higher expected return—the value premium—as compensation for the risk of poor performance during downturns.

3. Hypothesis 2: The Value Premium Is an Opportunity Created by “Market Overreaction”

Behavioral economics views humans as imperfectly rational, systematically making mistakes due to psychological biases. This predictable irrationality is the core of the market overreaction hypothesis explaining the true cause of the value premium.

Price Distortions Created by Investor Psychology

Investors exhibit cognitive biases such as:

- Overreaction and trend chasing: They become overly optimistic about growth stocks (winners) with good news and excessively pessimistic about value stocks (losers) with bad news, pushing prices above or below intrinsic value.

- Loss aversion and overconfidence: Investors feel losses more acutely and hesitate to sell losing stocks, while overconfidently flocking to growth stocks with flashy stories.

Lakoniak, Schleifer, and Vishny (LSV) argued that value investing succeeds because it exploits other investors’ systematic errors. By buying undervalued value stocks discarded due to excessive pessimism and avoiding overhyped growth stocks, investors earn excess returns when market expectations revert to reality.

Case Study: Bank of America (BoA) During the 2008 Financial Crisis

A dramatic example of the market overreaction hypothesis is Bank of America during the 2008 financial crisis.

- Extreme pessimism: Amid fears of financial system collapse, BoA was labeled the “ultimate loser stock.” Investors priced in bankruptcy as the worst-case scenario, causing the stock to plummet.

- Result of overreaction: In 2009, the stock price fell below $3 per share, with a PBR of about 0.2x—ignoring even liquidation value, a classic overreaction.

- Reversal of pessimism: Government intervention prevented the worst outcome, and as extreme fear subsided, the stock price recovered over several years. This reflected not a reduction in business risk but a normalization of excessive market fear.

Personally, I believe these two cases illustrate the dual nature of the value premium well. POSCO represents a strong case of “rational risk” compensation, while BoA during the financial crisis was closer to an opportunity created by “irrational fear.”

Advertisement

Table 2: Key Metrics for Bank of America During the Financial Crisis

| Year | Stock Price (Low, $) | Approximate PBR |

|---|---|---|

| 2007 | 45.05 | ~1.5x |

| 2008 | 10.93 | ~0.5x |

| 2009 | 2.53 | ~0.2x |

| 2011 | 4.92 | ~0.3x |

| 2013 | 11.61 | ~0.7x |

Note: Approximate values based on disclosures during the period.

Comparison / Alternatives

Core Comparison of the Two Value Premium Hypotheses

The “risk compensation” and “market overreaction” hypotheses view the value premium through different lenses. Rather than one being definitively correct, it is likely that both factors interact.

Table 3: Summary of Competing Hypotheses on the Value Premium

| Aspect | Risk Compensation Hypothesis | Market Overreaction Hypothesis |

|---|---|---|

| Core Theory | Efficient Market Hypothesis (EMH) | Behavioral Economics |

| Key Proponents | Eugene Fama, Kenneth French | Werner De Bondt, Richard Thaler |

| HML Factor Meaning | Proxy for systematic risk | Proxy for price distortions |

| Investor Behavior | Rational | Irrational (psychological biases) |

| Source of Returns | Compensation for bearing risk | Correction of market errors |

Conclusion

The value premium debate offers deep insights into how asset prices are determined. Do you believe markets are rational, or do you think they are driven by psychology? Your answer will shape your investment philosophy.

- Key Point 1: The value premium is a complex result of both risk and psychology. Some stocks are cheap because they are truly risky; others are cheap due to irrational fear. Both forces intertwine to create the value premium.

- Key Point 2: The definition of “value” is evolving. As intangible assets like software and brands gain importance, traditional value metrics like PBR face challenges. This may partly explain the recent weakening of the value premium.

- Key Point 3: Understanding “why” a stock is cheap matters now more than ever. Simply investing based on low PBR is outdated. You must analyze whether undervaluation stems from rational risk or soon-to-correct irrational psychology.

Next Action (CTA): Re-examine the undervalued stocks in your portfolio. Are they bearing hidden risks, or are they misunderstood by the market? Answering this question is the starting point for modern value investing.

References

- Sisain Growth vs. Value Stocks: Where Would You Invest? [Capital Market Stories]

- Ulsan University Graduate School Risk and Return

- Korean Finance Association Estimating Size Premium and Cost of Equity in Korean Stock Market

- Konkuk University Chapter 4 Exercise Answers

- Namu Wiki Capital Asset Pricing Model

- YouTube CAPM Explained in 1 Minute

- Namu Wiki Efficient Market Hypothesis

- Wikipedia Behavioral Economics

- Namu Wiki Behavioral Economics

- Hankyung Economic Terms Dictionary Growth vs. Value Stocks

- Wikipedia Efficient Market Hypothesis

- Velog Fama-French Three-Factor Model

- Korean Securities Association What Explains Korea Discount and PBR?

- Chicago Booth Review The Value-Stock Premium Is Shrinking

- Investopedia Fama and French Three Factor Model Definition

- FnGuide Factor Portfolio Construction Methodology

- Scripbox Cyclical Stocks: Understanding and Investing

- TradingView POSCO Holdings Common Stock Trading Ideas

- Brunch Introduction to Behavioral Economics - The Meeting of Economics and Psychology

- CNN Business Bank of America Stock Falls Below $5