Why the ‘Margin of Safety’ Truly Saves Your Life in an Uncertain Era

“Everyone has a plausible plan—until they get hit.”

We really love making plans, don’t we? Every new year, we set financial goals and sketch out life blueprints. But honestly, do those plans ever go exactly as intended? Probably not. The key isn’t to blame ourselves when plans fail. The real insight is to accept from the start that all plans will inevitably go off course. As bestselling author Morgan Housel insightfully points out in The Psychology of Money, the most important part of any plan is the plan for when the plan doesn’t go as planned.

This is far from pessimism. It’s hardcore realism—wisdom that humbly acknowledges the massive role of luck and risk beyond our control. The most primal and powerful tool for navigating this sea of uncertainty is the ‘margin of safety (Room for Error)’. This isn’t just about leaving some spare cash. It’s a survival skill that deliberately creates a buffer between the worst-case scenarios that could happen and the worst you can actually endure.

So why do we so easily ignore this simple yet powerful concept? What psychological traps keep pushing us onto thin ice? In this article, we’ll explore the essence of the margin of safety across personal finance, engineering, military strategy, and corporate rise and fall. We’ll also discuss concrete psychological methods to not just understand but deeply embrace and embody this survival skill in our lives.

From Bridge Design to Battlefields, the Laws of Survival Are the Same

The ‘margin of safety’ isn’t just a penny-pinching trick for money. It’s universal wisdom embedded at the core of every complex system that must endure unpredictable stress.

The Engineer’s View: The Non-Negotiable Number, ‘Factor of Safety’

Let’s peek into the world of bridge engineers. They have an absolute concept called the ‘factor of safety.’ If a bridge has a factor of safety of 3.0, it means it’s designed to hold three times the heaviest expected load. Wasteful? Not at all. It’s the humblest admission of human limits in perfectly predicting the future. Unexpected heavy rains, tiny material cracks, unknown ground shifts—engineers know these ‘unknown unknowns’ always exist. The factor of safety is the minimum respect we pay to the unknown, a buffer that protects our lives. Our financial plans should be no different.

The General’s View: The Last Winning Card, ‘Strategic Reserves’

The same applies in warfare. A skilled commander never reveals all their cards early. Consider the Battle of Kursk in WWII. Anticipating a massive German offensive, the Soviets built deep defenses and held their elite armored units as ‘strategic reserves’ in the rear. When the German spearhead dulled after repeated battles, these fresh reserves were unleashed for a decisive counterattack. The result? Complete control of the war shifted.

Your bank account’s “idle cash” isn’t lazy money eating away returns. It’s your ‘strategic reserve.’ When markets crash (the enemy shows weakness), while others panic-sell, you can boldly counterattack. When sudden job loss (an unexpected ambush) strikes, it’s the last fortress that keeps your life plan intact.

Advertisement

Why Do We Ignore the Margin of Safety? Hidden Traps in Our Brain

If it’s so rational, why do we keep walking on thin ice? The reason lies in a systematic bug built into our brains: ‘cognitive biases.’

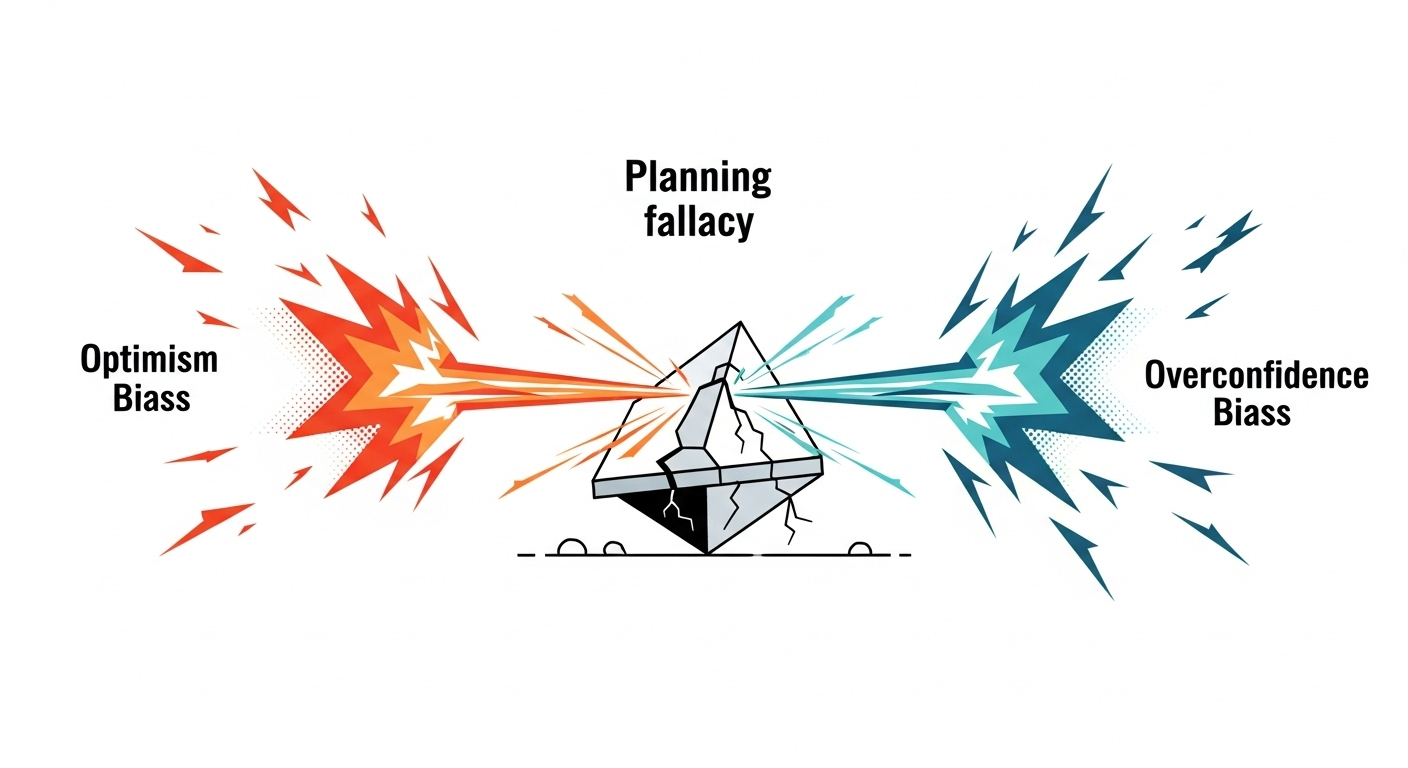

Planning Fallacy: The Optimistic Architect Within

As psychologist Daniel Kahneman revealed, we suffer from the ‘planning fallacy’—a chronic tendency to underestimate the time, cost, and risks needed for future tasks. The Sydney Opera House is a perfect example. Originally planned to be built in 6 years for $7 million, it took 16 years and cost 15 times more due to countless unforeseen issues. Aren’t we the same? Despite many past delays, we whisper, “This time will be different,” and make overly tight plans.

Optimism and Overconfidence: “That Won’t Happen to Me”

Two fuels make the planning fallacy even more dangerous: ‘optimism bias’ and ‘overconfidence bias.’ Optimism bias is believing bad things are less likely to happen to you (“I won’t get sick,” “I won’t have an accident”). Overconfidence bias is overestimating your abilities (“My investing skills are above average”). Combined, they cause us to ignore risks like job loss, illness, or market crashes and feel no need to build emergency funds. Especially when we ’trust our skills’ and take on unmanageable debt (leverage), ordinary risks quickly turn into catastrophic bankruptcy.

These cognitive biases feed on each other, creating a terrifying ‘vicious cycle’ that blinds us to the very concept of a margin of safety.

What Happens Without a Buffer Zone (Psychological and Financial Vicious Cycles)

Lacking a margin of safety isn’t just about being short on money. It erodes our mental state, paralyzes rational judgment, and pushes us into an inescapable downward spiral.

The Downward Spiral

For someone living without a buffer, sudden job loss isn’t just a financial issue—it’s a crushing loss of control over life. Extreme stress triggers ’tunnel vision,’ narrowing focus so much that there’s no energy left to consider long-term solutions. All mental resources go into just covering next month’s credit card bill. This often leads to stress-induced impulse buying or outright ignoring bills—‘financial avoidance’—making things worse.

Advertisement

The Betrayal of Leverage: The Orange County Bankruptcy Story

A textbook case of what happens when a large organization ignores the margin of safety is the 1994 Orange County bankruptcy. Treasurer Robert Citron massively leveraged debt, betting everything on a single scenario: interest rates would keep falling. But when the Fed raised rates in 1994, his unprotected portfolio suffered an unimaginable $1.6 billion loss, ending in the largest municipal bankruptcy in U.S. history. This tragic event painfully illustrates how overconfidence-fueled leverage can turn normal market fluctuations into disaster.

The Power to Turn Crisis into Opportunity: Margin of Safety and Resilience

But the margin of safety isn’t just a passive shield against the worst. It’s an active source of strength that turns crises into growth opportunities. At its core lies ‘psychological resilience.’

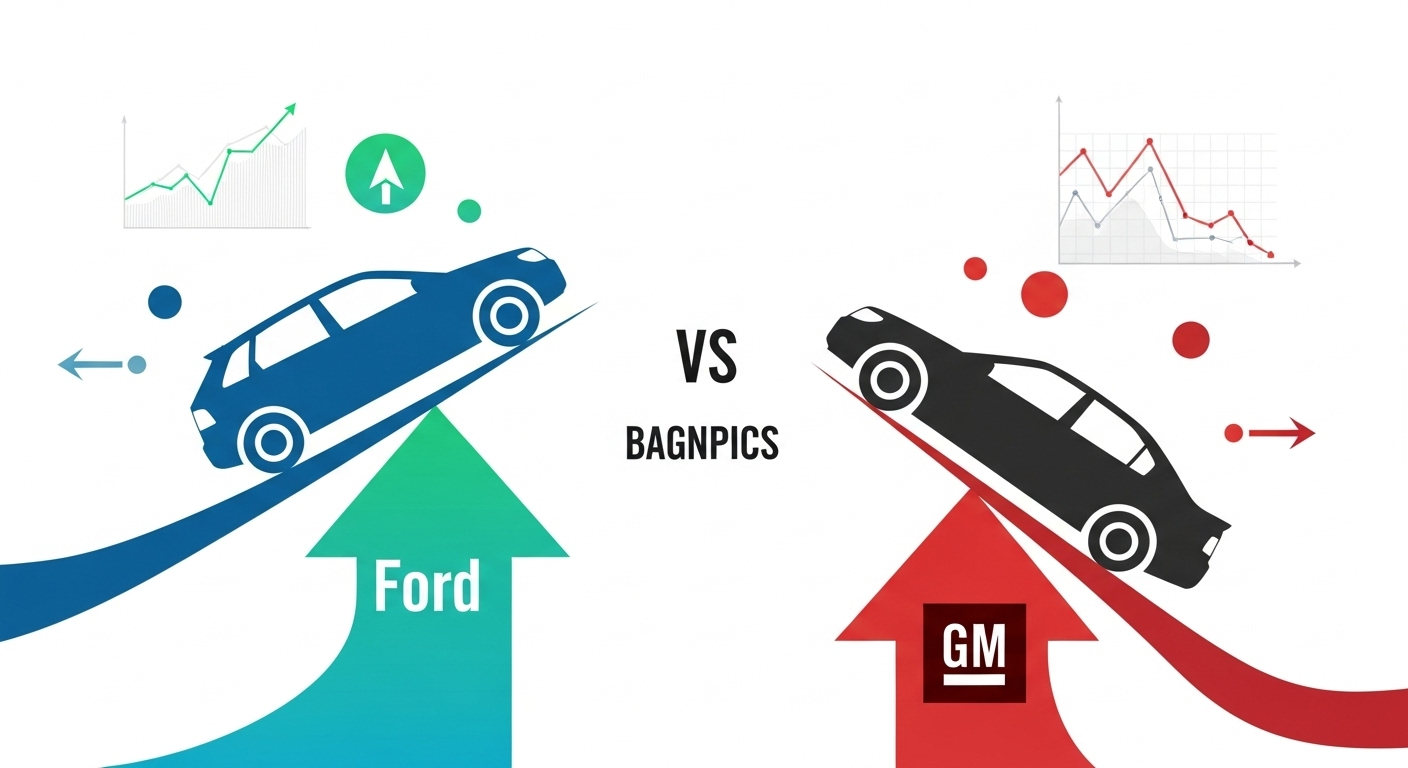

The 2008 Financial Crisis: The Divergent Fates of Ford and GM

The most dramatic example of how margin of safety determines corporate fate is the 2008 financial crisis story of Ford and GM. Two years before the crisis, in 2006, Ford CEO Alan Mulally borrowed a staggering $23.6 billion against all company assets, stockpiling massive cash reserves. Critics questioned why he went so far, but this move ultimately became the company’s **“masterstroke.”

When the financial markets froze in 2008, GM, lacking cash reserves, had to seek government bailouts and file for bankruptcy protection. Ford, however, survived without government aid thanks to its cash buffer and even continued investing in new car development amid the crisis. As a result, Ford increased its market share post-crisis. Ford’s margin of safety made it ‘financially unbreakable,’ turning a historic economic crisis into a prime opportunity to outpace competitors.

Thus, the margin of safety is both a shield to endure uncertainty and a spear that leverages it to leap higher than others—a most powerful strategic asset.

Practical Ways to Overcome Psychological Traps and Build Your Margin of Safety

Our brains are instinctively wired to ignore the margin of safety. To overcome this, conscious strategies and systems are essential.

- Conduct a ‘Pre-Mortem’: When making important financial plans, close your eyes and imagine, “One year from now, this plan has catastrophically failed.” Write down as many specific reasons as possible. Instead of vaguely asking, “Will it succeed?” ask, “If it already failed, why did it fail?” This quiets optimism bias and makes potential risks more vivid.

- Use the ‘Three-Point Estimation’ Technique: Don’t settle on a single goal. Consider three scenarios: the best case (optimistic), the worst case (pessimistic), and the most likely. Base your plan on the worst-case scenario. Intentionally injecting pessimism at the planning stage balances your outlook.

- Revere ‘Reasonless Savings’: As Morgan Housel emphasizes, beyond savings for specific goals like “wedding” or “house down payment,” you need savings with no reason at all. The biggest shocks in life always come from places we never imagined. This ‘reasonless money’ is the ultimate margin of safety against unknown risks.

- Trust Systems, Not Willpower: Resolutions like “I’ll spend less” rarely last beyond a few days. Willpower has clear limits. Instead, set up automatic transfers to savings or investment accounts as soon as your paycheck arrives. Moving savings from the realm of “decision” to “default execution” is the most reliable and powerful way to steadily build your margin of safety without emotional interference.

Conclusion: The Psychology of Wealth for Patience, Not Prediction

Building a margin of safety is a wise attitude combining humility about the unpredictability of the future, caution that things can always worsen, and long-term optimism that simply surviving will let compound interest work its magic.

Ultimately, financial success isn’t about hitting the highest returns. It’s about having ‘financial resilience’ that keeps your life intact no matter what crisis hits. In the long game of wealth building, endurance is the single most important skill that outshines all others. The margin of safety is the unique lifeline that guarantees we can endure that time.

Advertisement

Don’t try to predict. Just prepare to survive any wave without breaking. This is the most urgent, real psychology of wealth for living in a world full of volatility.

References

- Housel, Morgan. The Psychology of Money.

- Kahneman, Daniel. Thinking, Fast and Slow.

- Buehler, Roger; Griffin, Dale; Ross, Michael (1994). “Exploring the ‘planning fallacy’: Why people underestimate their task completion times.” Journal of Personality and Social Psychology. 67 (3): 366–381.

- Major media reports and historical analyses on the 2008 financial crisis, Orange County bankruptcy, Battle of Kursk, Sydney Opera House construction

- Literature on engineering and military strategy (factor of safety and strategic reserves concepts)